》View SMM Aluminum Product Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

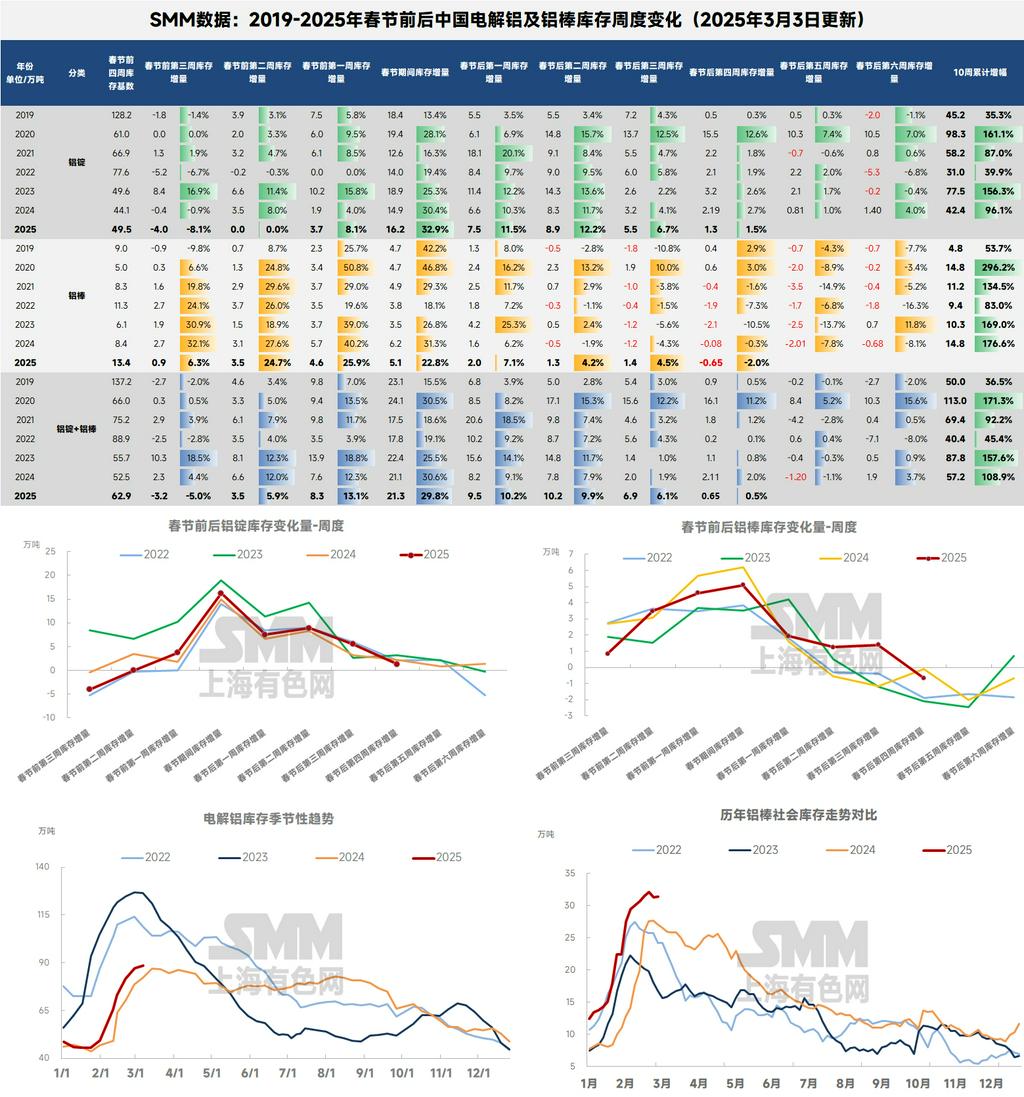

In late February, domestic aluminum inventory still showed no significant improvement, with inventory buildup remaining on the "fast track." The recent upward trend in aluminum prices has also been somewhat hindered by inventory performance. According to SMM data, as of February 24, 2025, the total social inventory of domestic aluminum ingots and billets rose to 1.194 million mt, surpassing the key thresholds of 1 million mt and 1.1 million mt consecutively, and is now approaching the 1.2 million mt mark. Specifically, inventory surged 69,000 mt WoW (up 6.1%), increased by 266,000 mt compared to the first day after the holiday (February 5), and accumulated an increase of 479,000 mt compared to the pre-holiday baseline (January 27). On a YoY basis, the inventory buildup in the third week after the holiday ranked among the top in terms of both volume and growth rate over the past seven years.

For aluminum ingot inventory, despite liquidity recovery in the market after the Lantern Festival and a slight increase in aluminum ingot outflows from warehouses over the past week, SMM statistics show that aluminum ingot outflows from warehouses totaled 119,100 mt in the past week, up 7,600 mt WoW; however, domestic aluminum ingot inventory continued its post-holiday buildup momentum. According to SMM data, as of February 24, 2025, the social inventory of domestic aluminum ingots reached 873,000 mt, with available inventory climbing to 747,000 mt, up 28,000 mt from last Thursday, showing no signs of slowing in the buildup pace. Notably, on a YoY basis, the inventory increase in the second week after the Chinese New Year exceeded that of the same period last year, with the buildup intensity ranking relatively high over the past seven years. The current inventory buildup slightly exceeded expectations.

SMM analysis suggests that although the current inventory accumulation is slightly above expectations (with inventory already surpassing last year's peak of 865,000 mt), the Q1 inventory peak is expected to be around 950,000 mt. However, with March approaching, downstream operating rates are expected to rebound steadily under the "Golden March and Silver April" seasonal demand boost, and in-transit cargo volumes in east and central China are already showing a downward trend. SMM predicts that the first destocking period this year is likely to occur in the sixth week after the holiday (around mid-March), similar to previous years. Close monitoring of resumption intensity, the release of in-transit cargoes, and the fulfillment of end-user orders will be necessary to adjust the timing and peak level of the inventory turning point.

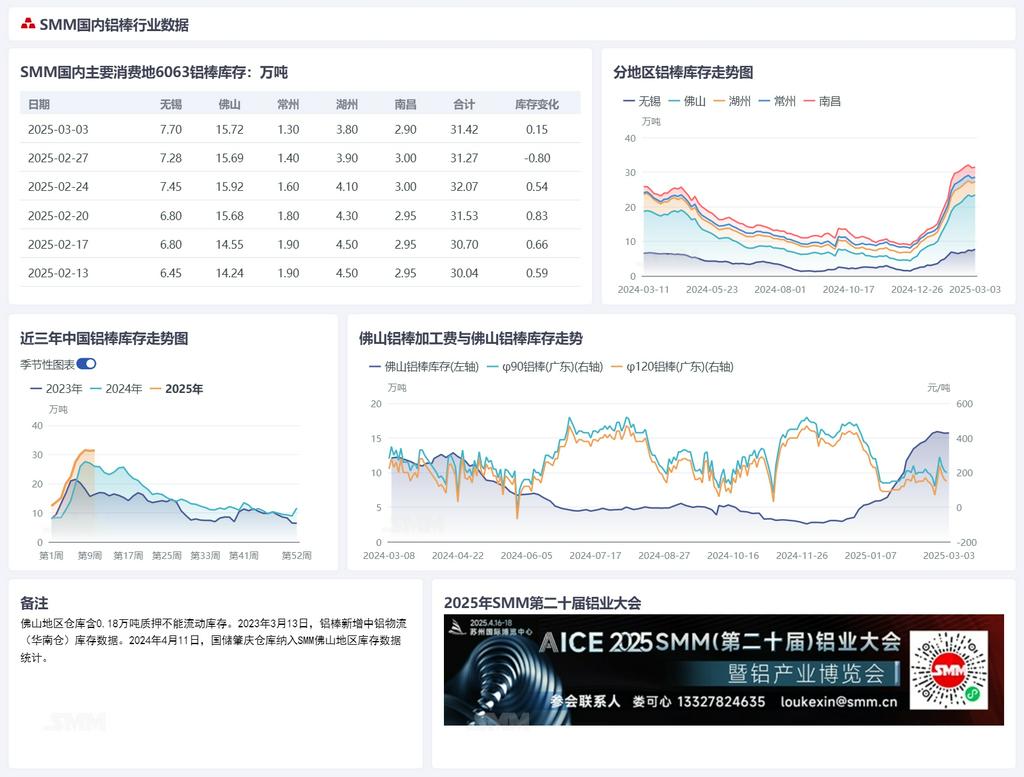

For aluminum billet inventory, according to the latest SMM data, as of February 24, 2025, the social inventory of domestic aluminum billets reached 320,700 mt, up 5,400 mt WoW. The overall inventory buildup rate remains manageable, with Wuxi, Foshan, and Nanchang ranking as the top three contributors to the buildup. Notably, the accelerated resumption of downstream extrusion plants after the Lantern Festival drove a rebound in outflows from warehouses, with the past week's outflows totaling 51,500 mt (up 7,300 mt WoW), setting a new high for the year. Although some aluminum billet manufacturers may have adopted volume discounts, this still reflects a certain degree of end-user restocking demand. Based on the inventory evolution patterns over the past seven years after the Chinese New Year, SMM predicts that the inventory turning point for aluminum billets is likely to appear earlier than that for aluminum ingots, with the turning point expected to occur by late February or early March. The Q1 inventory peak is projected to be around 350,000 mt. With the traditional "Golden March and Silver April" peak season approaching and downstream operating rates continuing to recover, the market is closely watching the actual impact of consumption recovery on the destocking process.

On the demand side for aluminum billets, the overall operating rate of the domestic aluminum extrusion industry was 69.5% over the past week, remaining flat WoW. In specific segments, leading enterprises in the industrial extrusion sector maintained high operating rates. Automotive extrusion companies had sufficient orders, with new capacity gradually being released. The outlook for PV extrusion enterprises remains positive, with SMM surveys indicating that major enterprises saw steady order growth, primarily driven by seasonal increases in production plans. Notably, the newly introduced PV grid connection policy has yet to significantly impact the industry, and no large-scale rush for installations has been observed in the market. In the architectural extrusion sector, leading enterprises quickly resumed operations, leveraging their orders on hand, while residential-related orders remained relatively weak, and commercial projects such as industrial parks accounted for a higher proportion. Overall, despite some divergence among sub-sectors, the industry's comprehensive operating rate remained stable. SMM will continue to monitor inventory trends, changes in downstream demand, and the impact of industry and regional policies.